10 Aug

Background Check

The Impact of Incorrect Employment Background Checks

Read moreRead more

Someone else's mistake is on your credit report. Our attorneys will make them fix it, and pay for it.

With decades of experience in consumer protection law, Fair Credit Attorneys have secured millions of dollars for our clients. Our dedicated approach ensures that every client feels supported and confident as we navigate the complexities of credit reporting on their behalf.

At Fair Credit Attorneys, we promise tangible results. Leveraging decades of legal experience, we rectify credit report errors and inaccuracies.

Our transparent approach and effective action deliver positive outcomes for your financial future.

For litigation we operate on a contingency fee basis. This means you pay no upfront costs or out-of-pocket fees for our legal services.

Our compensation is directly tied to our success in securing a favorable outcome for you.

Our vetted team of attorneys has successfully won cases and collected payments for clients in almost all 50 states.

We’ve litigated against Fortune 100 companies in complex litigation with millions of dollars at stake.

If you've dealt with errors on your credit report, you may have considered a credit repair company. Here's what they won't tell you: there's a federal law that gives you far more powerful options, but only if you work with a licensed attorney.

No upfront fees. Ever.: We only get paid if we win. You pay nothing out of pocket.

Files formal legal demands: A demand from a licensed attorney carries real legal weight. Bureaus respond differently.

Can sue under federal law (FCRA): If your rights were violated, we take Equifax, TransUnion, or Experian to federal court.

Can recover money damages for you: Under the FCRA, you may be owed actual damages, statutory damages, and attorney's fees, paid by them.

Real legal leverage: Equifax and TransUnion have legal teams. So do we. That changes the conversation entirely.

Charges monthly fees: Typically $79 to $149 per month, often for months with little to show for it.

Sends dispute letters only: Anyone can send a dispute letter. Bureaus know this, and often ignore them.

Cannot file a lawsuit: Not licensed to practice law. When bureaus ignore them, they have no legal recourse.

You get nothing for the harm caused: Even if the error is removed, you receive no compensation for lost opportunities or damaged credit.

No legal leverage: Bureaus know credit repair companies can't sue. They act accordingly.

The Fair Credit Reporting Act (FCRA) is a federal law that gives every consumer the right to an accurate credit report, and the right to sue when bureaus or creditors fail to fix legitimate errors. Credit repair companies cannot invoke this law. Licensed attorneys can.

Actual damages

Statutory damages up to $1,000

Punitive damages

Attorney's fees paid by the defendant

You could be owed compensation under federal law. If you read even one of these and thought "that's me," there's a real chance you have a case. Our attorneys review your situation for free and tell you honestly whether you do.

Maybe it belongs to someone with a similar name, or it's the result of identity theft. Either way, a debt you never created is sitting on your report and dragging your score down through no fault of your own.

You settled it. You have the receipts. But the creditor or bureau never updated the record, and now lenders are seeing a balance that hasn't existed in months or years.

Sometimes after a debt is sold to a collection agency, both the original creditor and the new collector report it separately. One debt becomes two strikes against you.

Most negative items have a legal expiration date, typically seven years. When they stay on your report past that point, it's not just unfair. It may be a violation of federal law.

This happens more than most people realize, especially with common names. Someone else's bankruptcy, late payments, or collections get mixed into your report and treated as yours.

You caught the error, filed a dispute, and the bureau or creditor investigated, then confirmed the wrong information anyway. That failure to correct a known error is one of the strongest grounds for legal action under the FCRA.

Find out in a free 15-minute attorney review.

No obligation. No upfront cost. A real attorney reviews your situation.

Contact us for a free consultation. We’ll thoroughly review your credit reports to identify any errors impacting your financial health, with no upfront fees.

We’ll send letters to dispute inaccuracies with credit bureaus and furnishers on your behalf. Our goal is to resolve issues quickly without a lawsuit.

If disputes fail, we’ll file a lawsuit to fix errors and seek damages for you. Payment is contingent on a successful outcome, ensuring your credit issues are fully resolved.

Are you seeing something on your credit report that just doesn't look right? Even a small mistake can have a big impact on your financial life, affecting everything from loan approvals to interest rates. We're experts at identifying and rectifying inaccurate credit report entries, working to ensure your report is fair and accurate. Let us help you clear up those frustrating discrepancies and get your credit back on track.

Whether it's for a new job, housing, or other important opportunities, a background check should always be accurate. Unfortunately, errors can occur, leading to missed opportunities. We specialize in helping you dispute and correct inaccuracies on background checks, ensuring your public record truly reflects who you are. Don't let someone else's mistake hold you back.

A mixed credit report happens when your information gets jumbled with someone else's – sometimes even someone with a similar name. This can lead to a credit report that's completely wrong and damaging. Our team is skilled at untangling these complex mixed file issues, meticulously working to separate your accurate information from another individual's data, so your credit profile is truly yours.

Landing that dream job often depends on a clean employment background check. If there are mistakes on your report, it could cost you an opportunity. We're here to help you challenge and fix errors on employment background checks, ensuring your professional history is accurately represented and doesn't unfairly hinder your career prospects.

In today's digital world, identity theft is a serious and growing threat. If your identity has been stolen, it can wreak havoc on your credit and financial standing. We provide legal assistance to help you navigate the aftermath of identity theft, working to remove fraudulent accounts and activities from your credit report and restore your financial integrity. Let us help you fight back and reclaim your identity.

Discovering a credit card denial due to report errors is frustrating, especially when you know your financial history is solid. Inaccurate information on your credit report can seriously damage your ability to get approved for new credit. Common mistakes include wrong account balances, duplicate accounts, or even identity theft. These errors can drag down your score, making you seem like a high-risk borrower.

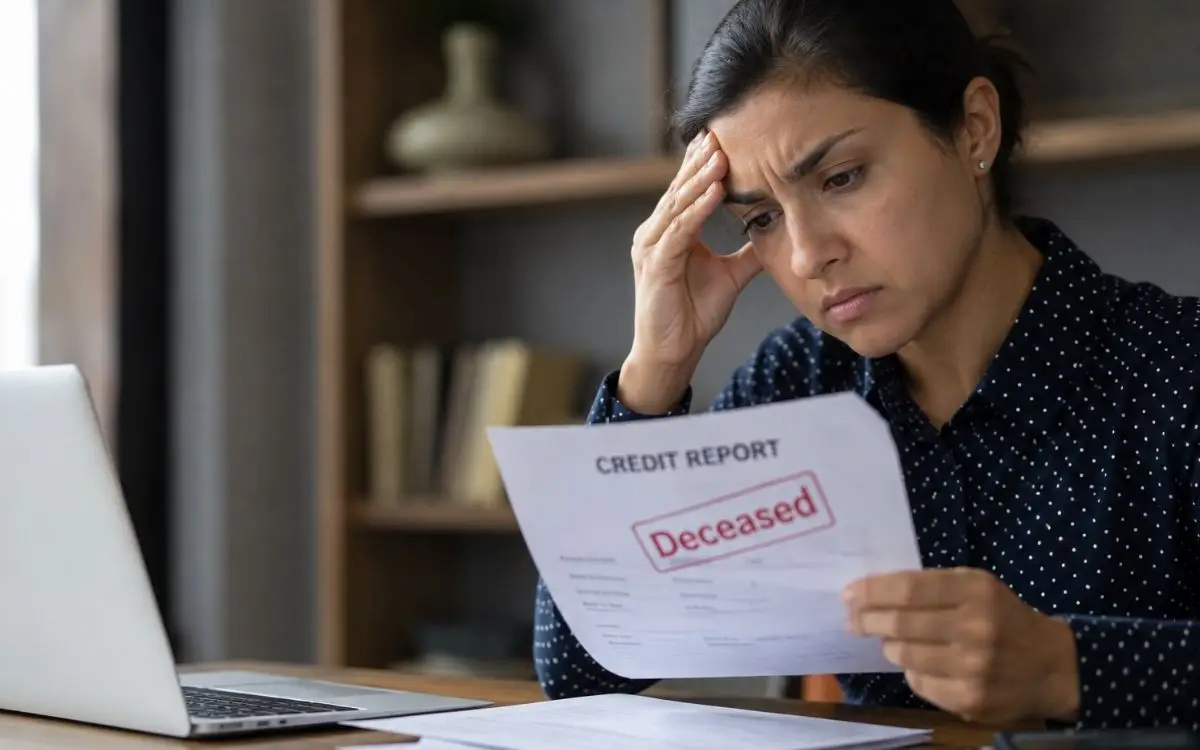

It's a shocking situation to discover a "deceased on credit report error." This grave mistake can bring your financial life to a grinding halt, freezing your accounts and preventing you from securing new credit. This typically happens when credit bureaus mix up consumer files or misinterpret data from the Social Security Administration. Correcting this error is a priority to regain control of your finances.

A mortgage denial due to credit errors is one of the most disheartening experiences for a prospective homebuyer. After months of searching, an inaccurate credit report can stop the process cold. Errors like misreported late payments, incorrect loan balances, or accounts that aren’t yours can unfairly lower your credit score, making you ineligible for a home loan.

Our dedicated team of attorneys brings a wealth of knowledge and passion for consumer protection. We are committed to providing personalized attention and unwavering advocacy for every client.

(+30 Reviews)

While we're rooted in Illinois, our expertise in consumer protection law and our commitment to rectifying credit report errors extends across the entire nation. We serve clients from coast to coast, bringing our 50 years of legal experience to bear on behalf of consumers wherever they are located.

Straight answers about credit report errors, your rights under federal law, and what working with a consumer protection law firm looks like.

A credit report error attorney enforces your rights under the Fair Credit Reporting Act (FCRA), the federal law that requires credit bureaus and creditors to report accurate information. We dispute the error, and if the bureau fails to fix it, we can file a lawsuit and seek damages on your behalf. Learn more about how our FCRA lawyers handle credit report errors.

Credit repair companies send dispute letters and charge monthly fees. They cannot file a lawsuit or recover money for you. As a consumer protection law firm, we can take Equifax, Experian, or TransUnion to federal court when they violate the law, and seek damages paid to you. You pay no upfront fees, and we only get paid if we win.

Nothing out of pocket. Your case review is free, and we only get paid if we win. The FCRA also allows courts to order the company that broke the law to pay your attorney's fees. Request your free case review to get started.

Common examples include accounts that are not yours, mixed credit files, identity theft, paid debts still showing as unpaid, outdated negative items, and background check errors that cost you a job or housing. If you disputed an error and it was not fixed, you may have a claim.

Under the FCRA, a credit bureau generally has 30 days to investigate your dispute, and in some cases up to 45 days. If it ignores your dispute or confirms false information anyway, that failure may violate federal law and give you the right to sue.

Yes. If a credit bureau violated your rights under the FCRA, you can bring a claim in federal court. Depending on the facts, you may recover actual damages, statutory damages, punitive damages, and attorney's fees. Our attorneys can review your situation for free and tell you honestly whether you have a case.